CALL US NOW

CALL US NOW EMAIL US NOW

EMAIL US NOWColorado state law does limit how long a debt can be pursued, but it’s important to note that you can still legally owe a debt even if it’s time-barred. The statutes of limitations governing debts can also be complex, and you can unknowingly reset the time a creditor has to collect a debt by making a payment or using an account.

Simply holding your breath and waiting for the deadline on debt to expire is not typically the best way to deal with any debt you may owe. If you can pay a debt and don’t feel like the creditor is stepping on your rights or charging you unfair interest or fees, it’s often best to clear the slate. That way you can work on rebuilding your credit and financial situation.

However, if you are struggling to pay a debt or you feel a creditor has stepped outside of the law to try to collect, it may be time to call a debt relief attorney. Find out more about how long creditors have to collect debts below and how an experienced lawyer can help you make your case.

What Is the Statute of Limitations on Debt in Colorado?

Colorado law considers debts time-barred after a certain amount of time. That time can range from three years to 20 years, and how long creditors have to pursue collections depends on the type of debt.

Here’s a basic run-down of the deadlines for different types of debts:

- On-account debts, which include things like mortgages, credit card accounts, and medical debts, have a statute of limitations of six years.

- Auto loan debts are an exception, and they have a statute of limitations of four years in the state.

- Oral and written contract debts that don’t meet the on-account definition have a three-year statute of limitations.

- Debts backed by a District Court judgment have a statute of limitations of 20 years.

What Date Is the Statute of Limitations Calculated From?

In many instances, the time period for the statute of limitations is calculated from the last activity on the account or the date that the account first became past due. It may depend on which occurred later.

For this reason, you can reset the statute of limitations if you make a payment on an account. For example, if you have a credit card account balance of $500 and you haven’t made a payment for five years, the statute of limitations would be up within the next year. However, if you make even a small payment in response to collections pressure, you can restart the clock and the creditor could have another six years to try to collect the rest of the debt.

Do You Still Owe a Debt After the Statute of Limitations?

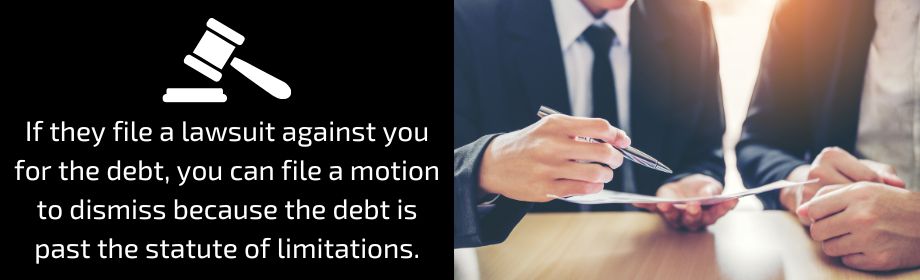

When the statute of limitations passes, the debt becomes time-barred. That means the creditor is not able to pursue the debt via a lawsuit. If they file a lawsuit against you for the debt, you can file a motion to dismiss because the debt is past the statute of limitations. As long as that’s accurate, the court would dismiss the case, which means the collector could not win the case and subsequently get orders to garnish your wages or put liens against your property.

That doesn’t mean you don’t still owe the debt, though. The collector may still contact you about the debt unless you request in writing that they stop. The debt may also still show up on your credit report, and it can keep you from future opportunities. For example, mortgage lenders may require that you pay off debts like this before you can qualify for a home loan—even if the debt is time-barred.

Understanding Your Rights as a Consumer

When it comes to debt collection, consumer rights in Colorado are protected by a number of state and federal laws. That includes the federal Fair Debt Collection Practices Act and the Colorado Fair Debt Collection Practices Act.

Some things collectors can’t do when pursuing a debt you might owe include:

- Calling you when you are at work and you have made known that you aren’t allowed to receive personal calls there.

- Calling you in a way that is harassing, such as making constant phone calls late at night.

- Discussing your debt or account with others without your express permission.

- Contacting you via phone after you have requested in writing that phone contact cease.

- Threatening you, including using obscene language, to try to scare you into paying the debt.

- Not providing basic information to verify the debt, including the name of the original creditor, when you ask for it.

How a Debt Relief Lawyer Can Help

If you’re facing a debt burden you can’t pay or you’re dealing with debt collection calls, an experienced lawyer can help. Contact the Holland Law Office today to find out more about your options, including protections like the automatic stay of bankruptcy or the potential for counter-suing creditors and collectors that have crossed legal lines.

If you’re dealing with a debt that may be time-barred, reach out today. We can help you understand the details of your case and how the statute of limitations might help (or hurt) it.